Jonathan Fullwood and Daniele Massacci

Episodes of vanishing market liquidity haunt dealers. This was true in the great stock market crash of 1929 and remains so today: in August 2018, professional corporate bond traders cited vanishing liquidity as their primary source of worry. Dealers in more-liquid long gilt futures – contracts on 10 year UK government bonds – might be less concerned. But have structural changes in the market led to less resilience over time? We address this question in a recent Staff Working Paper. We find that liquidity in the long gilt futures market has increased slightly over recent years, while remaining resilient to periods of market stress.

“The wires to other cities were jammed with frantic orders to sell. So were the cables, radio and telephones to Europe and the rest of the world. Buyers were few, sometimes wholly absent. Often the specialists stood baffled at their posts, sellers pressing around them and not a single buyer at any price.”

Three Years Down

Jonathan Norton Leonard (1939)

What is liquidity and why does it matter?

We can define liquidity as the ability to trade large amounts of a financial instrument quickly, at low cost and with little price impact. Traders clearly care about this, but so do firms and investors. This is because the liquidity of markets is linked to funding liquidity – the ability to raise cash by borrowing. More generally, market liquidity has economic benefits when it is reliable and resilient to stress.

The previous statement hints at an important issue for policymakers. It is not enough just to consider liquidity during normal times. Perhaps the most notable facet of market liquidity is that it can be elusive: ample liquidity in normal times can dry up when traders need it most. Policymakers worry about this.

Naturally, then, there is considerable interest in whether new regulations (such as the liquidity ratio) and changes in market structure such as growth in high frequency trading might have adversely affected liquidity conditions, either in normal times or during times of market stress.

We aim to measure liquidity in the gilt futures market to establish how it has changed over time, and its resilience during stress events.

Measuring liquidity

How should we measure liquidity? Simple proxies such as the bid price to ask price spread are not useful for futures on 10 year gilts. In such liquid futures markets, bid-ask spreads are often equal to the minimum allowed price increment – the ‘tick size’ – and thus effectively constant. When this is the case, bid-ask spreads give a false indication that liquidity conditions do not vary. The bid-ask spread also has another problem. If the volume of quotes at the best bid and best ask prices is small, then the bid-ask spread will give a false account of the cost of trading many contracts.

To get a better estimate of market liquidity we used the full order book for gilt futures (Figure 1). This let us calculate more useful measures of trading costs by allowing us to consider all price levels necessary to fill an order.

Figure 1: Schematic illustration of a limit order book with time priority. For multiple orders at the same price, the earliest is filled first

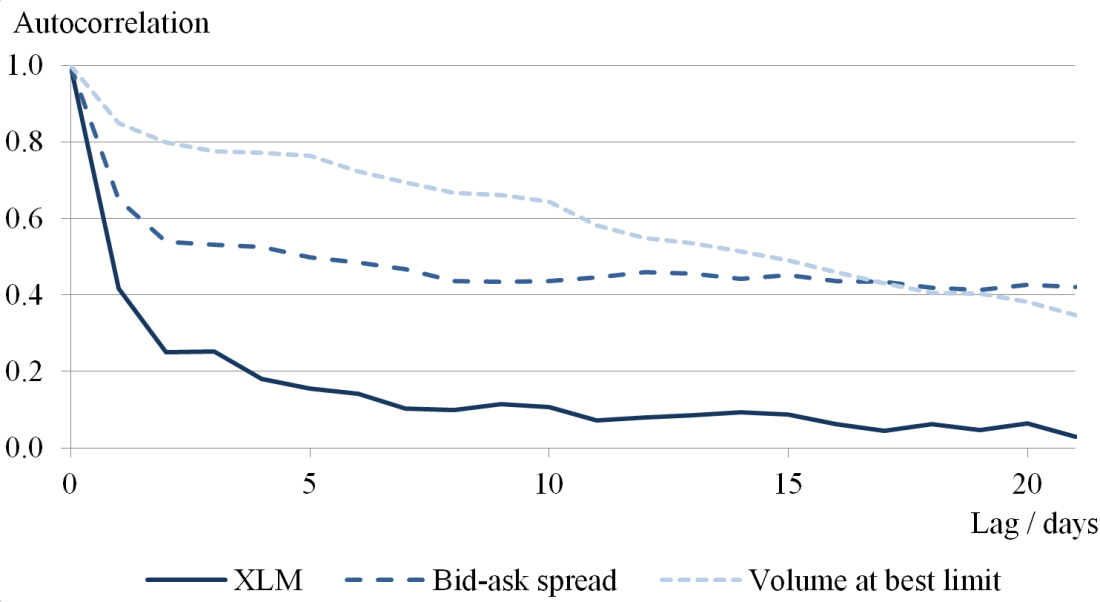

We settled on the Xetra liquidity measure (XLM) which represents a round-trip cost for a trade of a given size. A formal definition can be found in the working paper, but the XLM reports the total cost of buying and immediately reselling a given number of contracts. Using XLM had another benefit: autocorrelations for the measure were far lower than for simpler metrics (Figure 2). This is relevant when assessing resilience to adverse shocks because we may need to detect rapid changes in liquidity.

Our order book data ran from October 2014 to April 2017. We calculated our liquidity measure for order books at one minute intervals.

Figure 2: Autocorrelations for the XLM measure, bid-ask spread and volume at best limit for order sizes of GBP100 million

The relationship with funding liquidity

We began by studying the link between our market liquidity metric and funding liquidity – the “ability to raise cash by borrowing”. We used the gilt repurchase market as our proxy for funding liquidity and calculated three different liquidity measures for both specific and general collateral, as in Bicu et al. (2017).

We found that trading volumes in the gilt futures market tend to be lower when funding liquidity conditions have worsened. Funding and market liquidity meanwhile tend to be positively correlated. The degree of co-movement between the two tends to increase with trade size. We cannot infer anything about the direction of causality, but our findings imply that the market is likely to be more liquid in periods of abundant funding liquidity.

Liquidity trend

To estimate the long term trend in trading costs we considered one month rolling average liquidity. Fitting an autoregressive trend model produced a trend term that was slightly negative and consistent with being non-zero at the five percent level. That is, round trip costs appear to have declined slightly over the period of the analysis.

Liquidity resilience

To test the resilience of liquidity in the futures market we examined our measure at times of potential market stress. First we considered the Bank of England Asset Purchase Facility operations with the highest and lowest cover ratios. We were unable to discern any effect on gilt future liquidity around these times.

We also looked at two periods of market stress: the surprise removal of the euro to Swiss franc exchange rate floor in 2015 and the days following the EU membership referendum of 2016.

In both cases, trading costs increased sharply during the period of stress, but trades of GBP100 million remained executable given the liquidity in the order book. In the case of the Swiss franc de-peg, reversion to the unconditional average level of liquidity took less than one day. After the EU referendum the period of reduced liquidity was slightly longer, but long term average levels of liquidity were seen again within two trading days (Figure 3).

Figure 3: XLM round trip trading cost for GBP100 million on June 23rd, 24th and 27th, 2016

Final word

Despite changes in the regulatory regime and other structural factors, we do not observe a decline in liquidity in the gilt futures market over the period of interest. For round trip trading costs it does appear to be a case of ‘three years down’. This finding may be motivated by an adequate provision of funding liquidity. Of particular note is the resilience of gilt futures market liquidity to periods of market stress.

We acknowledge and thank Intercontinental Exchange for providing us with the data.

Jonathan Fullwood works in the Bank’s Advanced Analytics Division and Daniele Massacci works in the Bank’s Markets Intelligence & Analysis Division.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied.Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.