Philip Bunn and Alice Pugh

It has been well established that macroeconomic outcomes, such as recessions and unemployment, can have important impacts on households’ well-being. So it follows that monetary policy decisions can affect happiness too. In a recent working paper we use a novel approach to assess how the unprecedented loosening in monetary policy in response to the 2008 global financial crisis affected the well-being of UK households. The framework we use could be used to assess the welfare implications of other monetary policy responses, including to the spread of Covid-19 during 2020.

Following the financial crisis, the Bank’s Monetary Policy Committee cut short-term interest rates from around 5% to close to zero, and launched a Quantitative Easing (QE) programme which purchased £375 billion of assets by mid-2012. These large interventions prompted a debate about the effects of monetary policy on inequality. Most studies have found the effects to be small. However, these relate to measured income and wealth rather than broader measures of well-being which ought to be what matters most to individuals.

We look beyond the effects of monetary policy on income and wealth to the effects on well-being. We find that changes in monetary policy since 2007 raised the well-being of most UK households, relative to what would have happened. But because overall well-being fell after the financial crisis, the effect of monetary policy was to mitigate the extent of this fall rather than boost well-being in absolute terms. Strikingly, much of this relative welfare gain came through non-financial, rather than the conventional financial (income and wealth) channels. The lower incidence of household unemployment and financial distress than would otherwise have been the case is estimated to account for 80% of the overall welfare gain. Failure to account for these channels could substantially under-estimate the benefits of supportive monetary policy.

As always there are some caveats to point out. The results are dependent on how well-being is modelled, which we explain in more detail below. Our study is an event-study exercise focused on the monetary policy response to a single event – the global financial crisis. It is not an assessment of policy decisions relative to equilibrium real interest rates (which are likely to have fallen; see Box 6 in the August 2018 Inflation Report) or of the implications of monetary policy decisions over the business cycle. Nor does it consider the welfare gains from the current inflation targeting framework.

What determines household well-being?

Many things will influence households’ well-being, including family relationships, living arrangements, health and personal finances. Monetary policy will have notable effects on a subset of these factors, in particular income, wealth, employment and ability to make debt repayments. The first step in our analysis is to assess the strength of the relationship between the main factors that monetary policy can influence and household well-being. We estimate a household-level utility function of the form:

𝑈 = ∅(𝛼(𝑦), 𝛽(𝑤), 𝛾(𝑋))

where 𝑈 is utility, 𝑦 is income, 𝑤 is wealth and 𝑋 includes variables other than income and wealth. We can use this specification to assess: the relative weight households place on current versus permanent income (wealth), 𝛼 and 𝛽; which variables other than income and wealth, 𝑋, affect household well-being and with what weight, 𝛾; and the curvature of the utility function (degree of diminishing marginal utility), ∅.

We follow the survey-based approach of Layard et al (2008) and estimate the utility function using data from the longitudinal Wealth and Asset Survey (WAS). Since 2011, respondents to the survey have been asked to rate aspects of their own well-being (life satisfaction, happiness, anxiety and the extent to which life is worthwhile) on a scale of 0 to 10. We use these responses to approximate household utility, 𝑈. We are able to include a range of individual-level controls (for example age and marital status) in our analysis, as well as household-level fixed effects.

Our findings are as follows:

- Both current income and wealth (permanent income) affect household well-being.

- Not all types of wealth are important. Physical, financial and deposit wealth enter significantly in the utility function, but pension and housing wealth do not, perhaps because they cannot easily be observed by households and used to finance consumption.

- Non-financial factors such as unemployment and being in financial arrears have a large impact on well-being. This is a well-established finding in the literature. These factors are estimated to be much more important for well-being than income or wealth.

- The relationship between well-being and income and wealth is approximately log-linear (Chart 1). This implies that the marginal utility of income and wealth is diminishing, and that changes in happiness that arise due to changes in income and wealth are best captured in percentage, rather than in monetary terms.

Chart 1: Well-being and income

How does monetary policy affect well-being?

To assess the impact of monetary policy on welfare we also need estimates of how monetary policy has affected each variable in the utility function. To do this we draw on the results from Bunn, Pugh and Yeates (2018) who estimate the impact of monetary policy on the measured income and wealth of individual households in the Wealth and Asset survey. We supplement these with additional modelling of financial distress. By doing the analysis at a micro level we are able to assess how monetary policy affected the well-being of different groups of households as well as analysing the effects in aggregate.

Our findings

1. Monetary policy has boosted household well-being, mainly through lower unemployment and financial distress

Changes in monetary policy after 2007 are estimated to have raised average well-being by around 0.25% by 2012-14, or 0.02 units on the 0 to 10 scale (Table 1). While this sounds small, households’ well-being scores have remained broadly stable since the mid-1990s, only moving in a range of about 5%. And it is important to remember that this is a boost to well-being relative to what would have otherwise have happened. Unemployment and financial distress still rose overall during this period, but by less than they would have done without monetary policy interventions.

The benefits of looser monetary policy via lower unemployment and financial distress are estimated to have been much larger than the boost via income and wealth, with the latter two channels accounting for only 20% of the overall boost to welfare (Table 1). This is consistent with unemployment and financial distress causing significant psychological damage. Our unemployment and distress effects relate only to the households affected. Some studies, for example Di Tella et al (2001), have also found evidence of a ‘fear of unemployment’ effect where the increased risk of job loss also reduces well-being for those who remain in work. Proxies for this were not statistically significant in our utility function estimates (once income and wealth were fully controlled for) but we note that this could still be an additional channel that would increase the importance of these non-financial channels further.

Table 1: Effects of monetary policy changes since end-2007 on well-being in 2012-14

2. Monetary policy is likely to have made most households better off in well-being terms

We estimate that the majority of households were made better off by changes in monetary policy over the financial crisis. We define better (worse) off as a rise (fall) in well-being of at least 0.01% (-0.01%). This is equivalent to just over 1% of average annual income. 60% of households were better off under this definition (Chart 2), while 20% of households were made worse-off due to lower savings income. Chart 2 also shows that 4% of households saw very large rises in well-being due to monetary policy, of over 1%. These larger gains were due to the avoidance of unemployment or financial arrears.

Chart 2: Distribution of changes in well-being

3. The well-being benefits of monetary policy have been greatest for younger households

Younger households tend to have less secure jobs and larger debts, and so have benefited the most from monetary policy reducing the probability of unemployment and financial arrears (Chart 3). They also tend to have gained more in income terms as they are more likely to be in work and to be net debtors, meaning that they benefited from lower interest rates on their debt payments.

Chart 3: Effects of monetary policy changes since end-2007 on well-being, by age

The well-being of older households has been left broadly unchanged by monetary policy, on average (Chart 3). Older households tend to be less exposed to changes in the risk of unemployment and financial distress, since they tend not to be in work or to hold much debt. They also lose out, on average, from lower deposit receipts (since they tend to be net savers). And while they gain from higher wealth, wealth is estimated to be less important for well-being (Table 1).

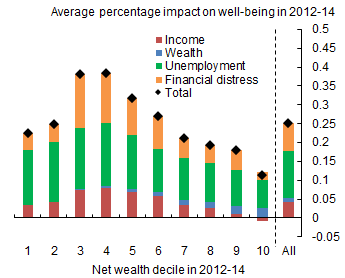

Split by net wealth rather than age, households in the bottom half of the wealth distribution are estimated to have gained more in well-being terms than those at the top (Chart 4).

Chart 4: Effects of monetary policy changes since end 2007 on well-being, by net wealth decile

Conclusion

Changes monetary policy after 2007 boosted the well-being of UK households, relative to what would otherwise have happened. Most of these benefits are due to the effects of lower unemployment and payment difficulties. Our results suggest that accounting only for financial channels (ie the effects of monetary policy on income and wealth) can substantially underestimate the benefits of monetary policy over the financial crisis period.

Philip Bunn works in the Bank’s Structural Economics Division and Alice Pugh works in the Bank’s Macro Financial Analysis Division.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.