Fergus Cumming.

As the UK economy went into recession in 2008, the Monetary Policy Committee responded with a 400 basis point reduction in Bank Rate between October 2008 and March 2009. Although this easing lessened the impact of the recession across the whole economy, its cash-flow effect would have initially benefited some households more than others. Those holding large debt contracts with repayments closely linked to policy rates immediately received substantial boosts to their disposable income. Cheaper mortgage repayments meant more pounds in peoples’ pockets, and this supported both spending and employment in 2009. In this article I explore one element of the monetary transmission mechanism that works through cash-flow effects associated with the mortgage market, and show that it can vary across both time and space.

Borrowing, spending and employment

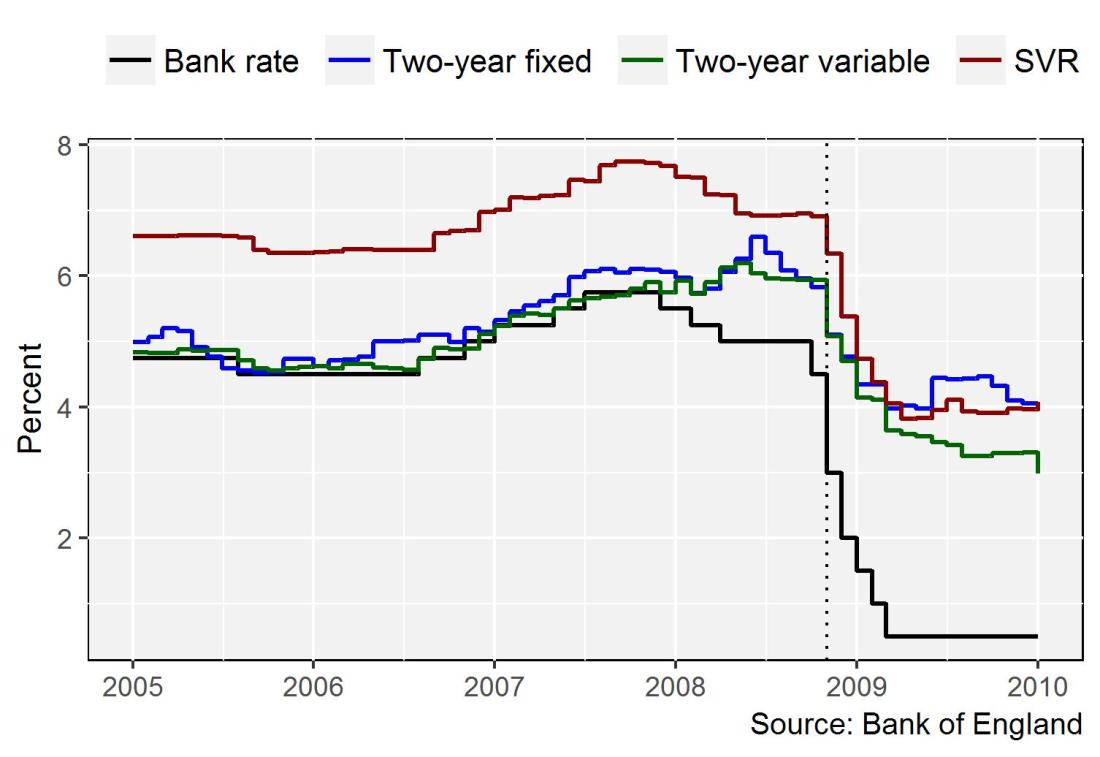

In a new paper, I estimate the employment impact of the dramatic cut in Bank Rate that occurred following the collapse of Lehman Brothers. Some mortgagors received a cash-flow boost as their monthly mortgage repayments fell in lock-step with policy rates as the nights closed in at the end of 2008 (Figure 1). Many chose to go out and spend part of this windfall, on goods made (and services provided) both at the national and local levels. And, as people finally got round to fixing their cars, made more trips to their nearby corner shop and splurged on meals out, we might expect this spending on locally-provided services to have supported local employment in the face of the Great Recession.

Figure 1: Mortgage interest rates

The first series shown is Bank Rate. From the Bank of England quoted rates series (with identifying code in brackets): 2-year fixed 75% LTV mortgage (IUMBV34), 2-year variable 75% LTV mortgage (IUMBV48) and the Standard Variable Rate (IUMTLMV).

Those who went into the autumn of 2008 with a mortgage linked to Bank Rate (on a so-called variable-rate mortgage) received an average favourable cash-flow shock equivalent to around 5% of their annual pre-tax income the following year: a large sum of money, equivalent to roughly the amount the average person saved every year. But those on fixed-rate deals were not so lucky; they often had to wait for their mortgage deal to expire to benefit from the cheaper financing conditions.

My results suggest that a 1 percentage point accommodative monetary policy change led to around a 3.5pp increase in annual employment growth of businesses that relied on local custom between 2009 and 2010. These businesses made up around a fifth of overall employment. This point estimate should be treated with caution and monetary policy operates through a number of channels that work over different horizons. There are also good reasons to think that the cash-flow effects I find would likely have been approximately symmetric if interest rates had instead increased. Nevertheless, the paper goes on to show that the joint spatial distribution of mortgage and labour market structures led to significant variation in the traction of monetary policy through the cash-flow channel across different parts of the UK in the Great Recession.

The universe of mortgages and employment

I estimate the employment effect of monetary policy through this cash-flow channel at a very granular level by combining datasets that contain more than 85% of mortgages and 99% of businesses. I first model the evolution of six million mortgage payment flows by taking information from the FCA’s Product Sales Database (PSD). This helps us understand how the 400bp interest rate cut affected almost every mortgaged household in the UK. I go on to estimate the change in each household’s income, relative to a world where rates had stayed north of 5%. I then aggregate these cash-flow shocks to the neighbourhoods immediately surrounding each of the 450,000 locally-facing businesses in the UK, whose details are listed in ONS-held administrative data. The key regression is of establishment-level annual employment growth in 2010 on the average cash-flow boost its customer base received in 2009.

There are three reasons why this simple regression captures the causal effect of neighbourhood cash-flow shocks on the employment behaviour of so-called locally non-tradable businesses. First, the PSD contains a great deal of information that can be used to condition the regressions successfully, and therefore minimises any risk of omitted variable bias. It is true that lower-income households are more likely to take out fixed-rate mortgages. But omitted variable bias only strikes when variables are omitted!

Second, I show that many households were as-good-as-randomly assigned a fixed or a variable-rate contract in the run-up to the Crisis. For many, the choice simply did not matter. In the Great Moderation the vast majority of mortgages had a contractual maturity of two years, after which it was common to refinance. Short contracts and a recent history of stable policy rates meant that many households did not focus their attention on how the contractual interest rate evolved. By the same token, households did not base mortgage choices on an anticipation of future monetary policy action. Survey evidence shows that only 10% of households in August 2008 expected policy rates to fall substantially in the coming months. In sum, households chose their mortgages based on a number of factors that varied over time; almost 40% of those who remortgaged between 2005 and 2008 switched between fixed and variable-rate contracts.

Third, the turbulence in the UK mortgage market, which accelerated after the failure of Lehman Brothers, restricted fixed-rate mortgagors’ ability to refinance their contracts in order to benefit from lower interest rates. A combination of high early-repayment fees, lower collateral values and short fixation periods meant that most fixed-rate mortgagors waited for their interest rate to reset rather than actively seek out a new contract. Unlike in the US, in the UK at most 7% of people on fixed-rate contracts actively refinanced their mortgages in 2009 based on total remortgaging activity during this period.

Policy across time and space

The overall impact on local employment through this cash-flow channel depended on both the make-up of the local mortgage and labour market. In parts of the country where there was a large proportion of variable-rate mortgages, people spent more in locally-facing businesses such as car garages, grocery stores and restaurants. The cash-flow channel of monetary policy was correspondingly weaker in parts of the country where there was a high proportion of fixed-rate mortgages, or where many people were employed in global industries such as car manufacturing and oil exploration.

Although UK unemployment rose by around 3pp in the year following the collapse of Lehman Brothers, the extraordinary monetary stimulus carried out by the MPC surely protected the aggregate economy from a fate far worse. Within that, some parts of the country were more exposed to the direct effects of monetary policy on household finances. But even for the least affected regions, I estimate that employment growth was around 1.4pp higher than it otherwise would have been solely through this channel (see minimum value in Figure 2).

Figure 2: The estimated impact of the 400bp cut in Bank Rate through the cash-flow channel

This figure is constructed by taking the establishment-level cash-flow semi-elasticity of employment and combining it with cash-flow shocks and locally non-tradable employment shares for each local authority. Colour breaks denote quartiles.

Ten years on, the mortgage and labour markets have evolved, which has interesting implications for the transmission of monetary policy. After a sustained period of mortgage rates close to zero, more than 90% of new mortgages are now fixed-rate contracts and so the average time-to-refinance on the stock of mortgages is increasing over time. Although the effects I estimate are likely to be approximately symmetric, the evolution of the composition of mortgages means that the direct pass-through of changes in Bank Rate to household finances is likely to be slower in the future.

Fergus Cumming works in the Bank’s Monetary Policy Outlook Division.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Nice post, well done !